Farming and Finances: Profit or Loss from Farming

Most people don’t start farming to crunch numbers and expenses. Like any business, even small-scale farmers need to consider their income and expenses.

In his chapter on economics, Mike Madison breaks down everything he reported on his Form 1040, Schedule F: Profit or Loss from Farming to give readers a good idea of what kind of accounting goes into farming (plus plenty of tips on how you can be more efficient with your funds!)

The following excerpt is from Fruitful Labor by Mike Madison. It has been adapted for the web.

There is a widespread tendency in our culture to view all human activity in financial terms—dollars acquired and dollars disbursed. At no other period in history have human values been so thoroughly monetized. I reject that view. For me, farming is not primarily about money.

It has more to do with an interesting and enjoyable way of living, and with having a useful role in my community (a community that includes not only humans, but also the other organisms with whom we share the region).

Nonetheless, I am forced to deal with the economics of farming as part of the reality of 21st-century life. The farm is our sole source of household income, and there have been years when an insufficiency of income has been inconvenient and stressful.

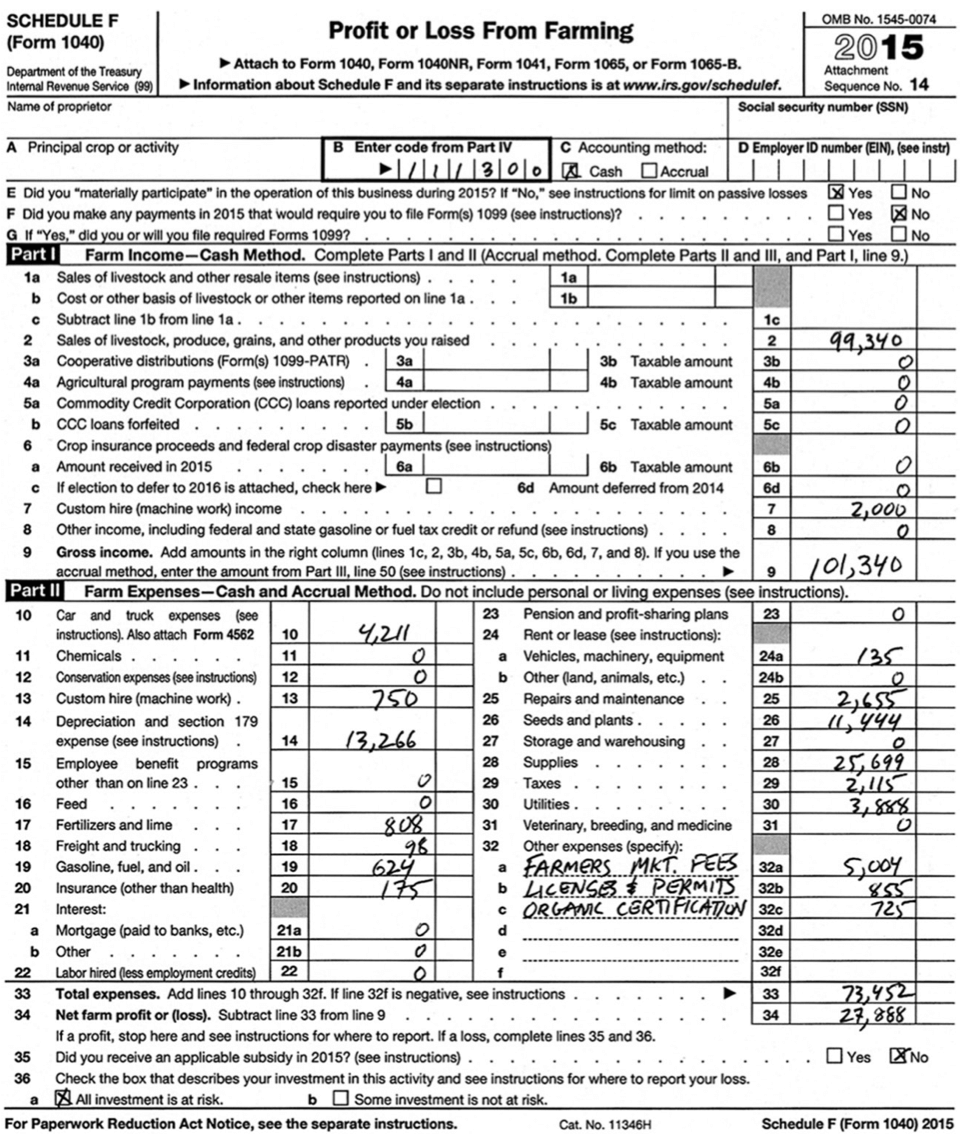

A good way to get a snapshot of the economic status of the farm is to look at the income statement that is submitted each year to the Internal Revenue Service. This is reported on Form 1040, Schedule F: Profit or Loss from Farming.

An example is given in the accompanying figure, and it is worth going over it line by line, as this will illuminate many of the economic aspects of farming.

Line 2: This is the gross income from sales, both retail and wholesale, of products produced on the farm.

Line 4a: According to the USDA census of agriculture, farms with gross incomes similar to mine receive, on average, $6,500 each year in direct subsidies from the federal government.

The subsidies are not distributed equally. They are as much political as economic, and they are heavily slanted toward commodity crops. Specialty crops such as those that I grow are not subsidized.

I am eligible for a partial refund of the $725 fee that I pay for organic certification through a USDA organic program grant. In the past I sometimes took advantage of this, but I no longer do so.

The organic certification industry is a racket—another bureaucracy carried on the backs of farmers, and so some relief from those expenses seems fair. But this strikes me as an inappropriate use of funds from the public treasury, and I’m reluctant to take part in it.

I know farmers who make a deep study of federal and state programs, and grab every dollar that might be available to them.

My practice is the other way; I have not taken advantage of subsidies for solar power installation, conservation practices, development of value-added projects, efficient irrigation, and others of my farm activities that would be eligible for tax credits or grants.

Similarly, there have been years of low income when we were eligible for food stamps and other sorts of public support, but we have never enrolled in those programs.

My convictions on this topic are still somewhat fluid, but it seems to me that one should do whatever it is that is the right thing to do, and to accept public monies for it is irrelevant and dishonorable. (I also must confess to a certain element of laziness about completing all the paperwork that claiming public funds requires.)

Line 6: I do not use crop insurance—I just take my losses as losses.

Line 7: This income represents custom milling of 5 tons of olives for friends at $400 per ton.

Line 10: We are only 8 miles from our farmers market and from a supermarket where we sell our products, so our annual mileage for farm business is small. We know other farmers who log 500 miles a week or more trucking their produce to markets in the San Francisco Bay area. The dollar cost of trucking (as well as its time cost and ecological cost) is quite high in those circumstances.

Line 11: Chemicals. On conventional farms, this is a significant item of expense.

Line 13: This charge is for a contractor who brought in a chipping machine to chip all the prunings from the orchards.

Line 14: Depreciation. This includes machinery, tools, and buildings. It is somewhat fictional in the sense that a well-built and well-maintained building is actually increasing in value, not decreasing.

Line 16: Because we do not sell the eggs, but give them away, we cannot deduct the cost of feed for the chickens. Nor can we deduct the cost of feed for cats, even when they are kept primarily for rodent control.

Line 17: Compost and gypsum.

Line 18: This covers a repair part for the olive mill sent from Italy.

Line 19: Fuel for tractors and tools. Fuel for vehicles is covered in line 10.

Line 21: I have no debts, so I pay no interest. I understand that credit is a tool, but it is one that we do not use.

Line 24: Rental of a trailer and of a trenching machine.

Line 25: This includes expensive remedial work on a water well. Every year it seems that some major repair will be required. I don’t know in advance what it will be, but I know that something will break in a way that is costly to repair.

Line 26: We plant a lot of bulbs every year (tulips, iris, ranunculus, lilies, etc.), and also continue to add trees—primarily citrus and olives. Some seeds, such as hybrid flower seeds, may be very expensive.

Line 28: The majority of this is packaging: bottles, caps, capsules, jars, lids, labels, bags, and boxes. We have not found suitable domestic glass, and so the bottles for olive oil are imported from Italy. Customers return about 40 percent of the glass, which we are able to clean, sterilize, and re-use. Also included in this line are a hundred dozen other little things—work gloves, paper towels, mouse traps, saw chains, sugar for jam, etc.—that add up in the course of a year.

Line 29: This includes that portion of the property tax attributable to the farming business, as well as sales tax collected on taxable items (flowers) sold in the farmers market. When we sell a bunch of flowers for five dollars, the true price is $4.63 plus 37 cents tax. That tax must be remitted to the state.

Line 30: Electricity for pumping water, running the cooler, running the olive mill, and charging the electric truck. Lighting is all LED lights, and does not use much power.

Line 32a: The farmers market fees are based on a percentage of gross sales. They pay for management, trash pickup, insurance, utilities, and the like. The market is very well run, but expensively so.

Line 34: The net income (incorrectly called “profit” on the form) is only about one-quarter of the gross revenue. This is typical of farming operations whether they are large or small.

Beyond Schedule F

Elsewhere in Fruitful Labor, I summarized the hours of labor that we (two adults) expend annually on the farm at 6,073 (3,036 hours each). In the US, the current annual labor of a full-time job is 1,900 hours: 52 weeks of 40 hours minus vacations, holidays, and paid leave.

Elsewhere in Fruitful Labor, I summarized the hours of labor that we (two adults) expend annually on the farm at 6,073 (3,036 hours each). In the US, the current annual labor of a full-time job is 1,900 hours: 52 weeks of 40 hours minus vacations, holidays, and paid leave.

So our work on the farm adds up to somewhat more than three full-time jobs done by two people. I generally work about 350 to 360 days each year.

Dividing the net revenue of the farm by the hours worked gives an hourly wage of $4.59

At a time when the minimum wage in California is $11.00 per hour, scheduled to rise to $15.00 in the nearfuture.

Enforcement of a minimum wage does not apply to the self-employed, and an income below minimum wage is typical for small-scale farmers. So, based on Schedule F, the income from the farm pays a substandard wage, while the profit is zero and the return on investment is zero.

Although the amount of hours worked might seem excessive, by historical standards it is not. There are 8,766 hours in a year, which leaves each of us 5,730 hours outside of work for other uses.

And it’s worth noting that this is not some soul-crushing office job or factory job; this is pleasant, interesting, autonomous, meaningful work carried out under the open sky.

The hourly wage calculated from Schedule F is misleading and it is important to consider the inaccuracies that Schedule F engenders. For example, vehicle expenses are charged at a per-mile rate, currently about 56 cents.

But I purchased my vehicles used at a good price, I maintain them myself, and I drive conservatively, so that the true cost of operation is closer to 30 cents per mile.

The $4,211 vehicle expense listed on line 10 is in reality only about $2,200. Similarly, the depreciation of farm buildings is considered an annual cost, when in reality the buildings are increasing in value.

And since the buildings were paid for at the time they were built, the annual depreciation expense is hypothetical, and does not actually take any money out of our pockets in the current year.

A second point overlooked by Schedule F is that we grow a lot of our own food as part of the farming operation. In addition, we barter produce and olive oil for wine, avocados, strawberries, veterinary care, and a few other things.

In theory one is supposed to report the value of barter as income, but on this scale—mutual gifts among friends—the rule does not apply.

These activities represent income with a value of about $5,000 per year that does not show up on Schedule F because it is not monetized, and because the government has not yet tried to tax people for growing their own food.

Most important, though, is that much of our labor increases the value of the farm, and hence our wealth, without ever manifesting as income.

Most important, though, is that much of our labor increases the value of the farm, and hence our wealth, without ever manifesting as income.

For example, if I plant an orchard, and dig trenches for irrigation, and lay pipe, and plant each tree, and drive in a stake and tie off each tree, and prune the trees, and keep after the weeds, and trap gophers, all of this labor to establish the orchard is not rewarded with any income.

However, it has increased the value of the farm by somewhere between $3,000 and $6,000 per acre planted.

As it turns out, erecting buildings is the most profitable use of my time on the farm. When I do farm labor I’m replacing an $11 dollar per hour farm worker, but when I’m building I’m replacing a $50 per hour building contractor.

I built the building that houses the olive mill and jam kitchen for a total cost of $17,000 ($2,400 was the building permit) using mostly recycled materials.

This took me a year, fitting the labor in between my regular farming work. A contractor would have charged at least $100,000 to build that building. So I came out ahead by $83,000.

This does not show up as income, but it constitutes an increase in our wealth.

Our total cash outlay for our farm land, buildings, trees, and infrastructure, not adjusted for inflation, is approximately $200,000.

The current market value of our farm, if we were to sell it, is above $1,500,000. While nearly all of that increase represents inflation, some of it—perhaps $250,000—represents the value of labor applied to the farm that was never compensated as income.

In addition, the residual value of tools and machinery that have already been depreciated is about $80,000. We can conclude that our annual income is not as bad as it appears on Schedule F; we probably make minimum wage.

Recommended Reads

Lessons in Resilience: How to Plan a Successful Farm Business

You may like...

-

$25.00

$25.00 -

$35.00

-

$34.95

Recent Articles

Beets can be grown year-round and are a perfect, flavorful addition to meals. Get started on growing your own no-till beets with help from these tips!

Read More

Everyone loves a refreshing, nutritious drink…even your garden! Take your fermentation skills into the garden by brewing fermented plant juice.

Read More

Cows are the gold standard for milk production. They are the ultimate heroes of sustainable living! Explore the benefits of having a cow on your farm or homestead.

Read More

Thinking about building a greenhouse but worried about an uneven or sloped yard? Building a greenhouse on a slope offers a bonus: the ability to use gravity to harvest rainwater. Embrace the natural landscape and get ready to grow your garden dreams!

Read More

Ready to transform your gardening game? Revolutionize your gardening with permanent beds! They help improve soil health, ensure crop growth, and are extremely easy to design, even for beginners!

Read More